Macro Headwinds Strengthen Bearish Price Trajectory Across Industrial Metals

Gold Eyed Ahead of Key US Political Events

Industrial & Precious markets are watching key events coming out of the US, as Eurozone and Chinese weakening economic indicators act as a catalyst for an already dangerous turning point in the US economy. While fears of further rate hikes did act as a drag on Industrial Metals for the last few months, the added factor of the US Debt Ceiling has also become a significant event that could test Global Markets across all Asset Classes in the coming weeks.

The US Federal Reserve is facing increased pressure to slow or pause rate hikes in June, as market bets on further hikes fall to 30%. As US Congressional members continue their arguments around the US Debt Ceiling, the risk of default is becoming ever-present. According to Treasury Secretary Janet Yellen, the US has until the 1st of June to agree to a debt ceiling increase, otherwise, the US faces the risk of defaulting on its Bonds, an event foreseen as potentially cataclysmic to its reputation as the world’s top Reserve Currency supplier. However, the combination of potential slowing rates and a resolution of the Debt Ceiling issue could reignite renewed confidence in Global markets and could see a return in Commodity demand.

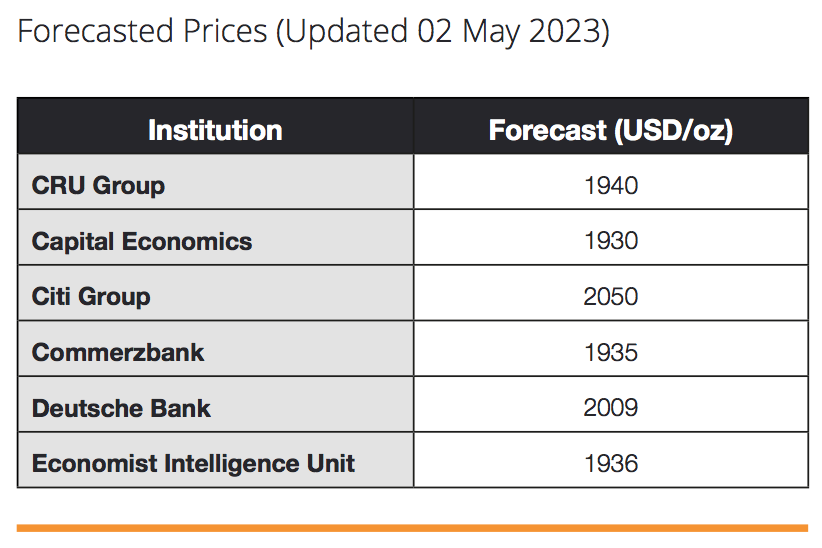

Gold

Gold prices face difficulty in building upward momentum despite some minor intraday upticks, encountering solid selling pressure around the $1,980/oz level. The precious metal retreated towards $1,970, halting the overnight recovery from last week’s monthly low.

Bearish market sentiment is largely being spurred by several Federal Reserve officials expressing hawkish views, leading to heightened expectations of future interest rate hikes. Consequently, market participants are now pricing in a 30% probability of a 25-basis points lift-off in June. This development acts as a catalyst for upward gold prices.

Support for XAU/USD stems from the lack of progress in discussions to raise the US debt ceiling and concerns about a global economic slowdown, which could lead to flights to safe havens. Negotiations between President Joe Biden’s representatives and congressional Republicans have yet to yield an agreement on increasing the government’s borrowing limit of $31.4 trillion. This has raised concerns about a potential default, further adding to the theory.

It is hard to be a bear during a recession when it comes to Gold. The bullish momentum of the US dollar remains a challenge for gold prices. Worries surrounding a slowdown in Eurozone business activity and disappointing macroeconomic data from China have reignited market concerns. These factors, coupled with expectations of sustained higher interest rates by the Fed, dampen demand for the Dollar-denominated metal. Developments in US debt ceiling negotiations and bond yields will be closely monitored as they directly impact the demand for the US currency. Additionally, overall market risk sentiment will contribute to shaping short-term trading opportunities for XAU/USD.

Moreover, the USD Index (DXY), which monitors the performance of the US dollar against a basket of currencies, remains stable, hovering close to a two-month high reached on Tuesday. This is primarily due to growing expectations that the Federal Reserve will maintain higher interest rates over an extended period. As a result, this could potentially erode the demand for gold priced in US dollars, as market participants anticipate the upcoming crucial release of the FOMC meeting minutes.

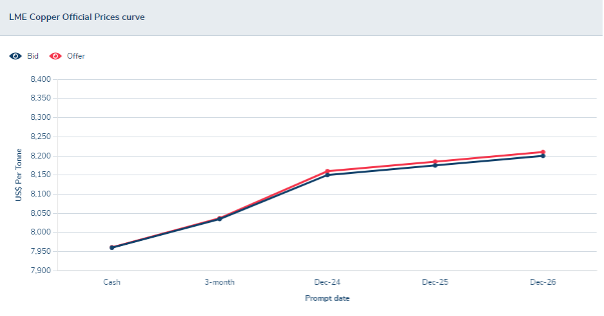

LME Copper

Further price weakness is being seen across the board in LME Non-Ferrous markets, the most notable mover being Copper, which has fallen to 5 1/2-month lows in recent weeks. Further concerns around weaker Chinese Economic data and further US Interest Rate hikes continue to drag prices lower, which is proving favourable to consumers but poses price risks to producers. Copper crossed the 200 moving average price on the 11th May 2023 and is continuing to trade within a range below that level. It’s important to note that lower energy prices have led to lower input costs for production and recessionary fears are not the only movers in price action.

According to analysts at Credit Suisse, if LME Copper fails to protect the level of 8070 there is a possibility of a more significant decline towards 7945, which is a 61.8% retracement from July 2022, as well as the key 7800 level. LME Copper has recently revisited the potential support zone around 8090, which combines a multi-month trend line, the lower boundary of a steep channel, and projections indicating a decline since January.

The formation of a bullish engulfing candlestick pattern on the daily chart suggests the potential for a rebound toward the upper limit of the channel, which is around 8450. sustained upward movement and indicate the possibility of an extended bounce.

LME Copper Forward Curve (Source, LME website)

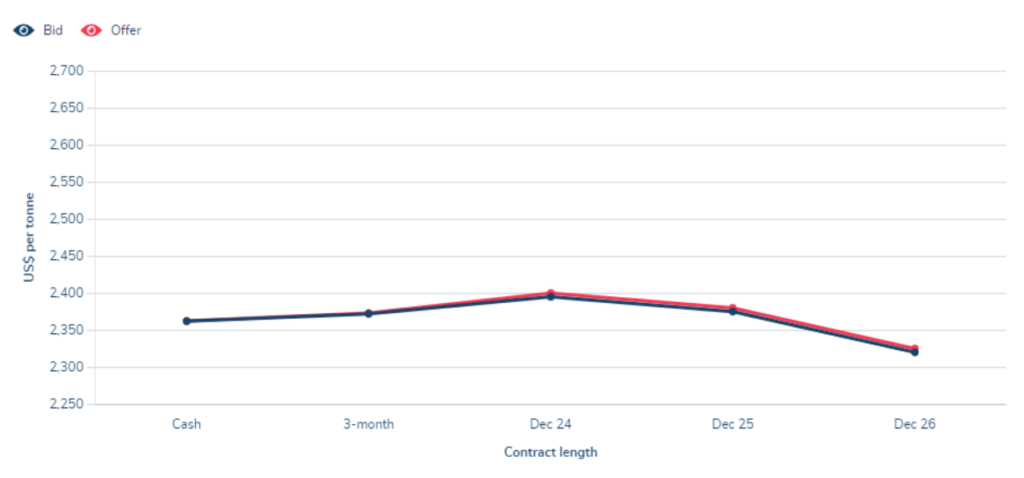

Zinc’s downward trajectory persisted, with prices dropping below 2,400 per tonne for the first time since October 2020. The decline can be attributed to sluggish demand and a surge in supply. Data from China, the largest consumer of zinc, revealed subdued demand in the world’s second-largest economy. Recent reports highlighted lower-than-expected retail sales, bank loans, factory gate deflation, declining imports, and reduced property investment.

On the supply side, China witnessed a year-on-year increase of 8.97% in zinc output in April, reaching 540,000 metric tons. Projections from SMM suggest that domestic refined zinc production in May is anticipated to grow by 8.65% year-on-year, totalling 559,800 metric tons. This growth is attributed to the completion of routine maintenance and the resolution of power supply issues in Yunnan.

Zinc

According to S&P Global forecasts, global refined zinc consumption is expected to witness a modest 1.3% growth in 2023, while global refined zinc output is projected to increase by a mere 1.9%. These figures reflect the subdued growth prospects for the zinc market amid the current demand-supply dynamics.

LME Zinc Forward Curve (Source, LME website)